|

Homework 4 Possible Solutions

K Foster, Options & Futures, Eco 275, CCNY, Spring 2010 |

|

|

- Please complete Assignment

Question 8.23 in

Stock price is 40. Euro 1-yr put with K=30 costs 7. Euro 1-yr call with K=50 costs 5. Investor buys 100 S, 100 puts, & short 100 calls, find profit/loss. What if 100 S, 200 puts, shorts 200 calls?

The Excel sheet shows the payoffs: with more invested in the options, the portfolio can make a higher return.

- Please complete Assignment

Question 9.23 in

Given c1, c2, c3

Euro calls with K1<K2<K3 and K3

K2 =

K1.

All have same maturity. Show c2

<= .5(c1 + c3)

. Hint: consider long c1, long c3,

short 2*c2.

Using

the formula for the lower bound on a call price, that ,

just substitute in

so

with K3 K2 =

K1 this is zero exactly.

- Please complete Assignment

Question 9.24 in

For puts?

Again

use the lower bound result that ;

substitute in for

- Please complete Assignment

Question 9.25 in

All company debt matures in 1 year; if value of company is greater than debt then pay off debt else bankruptcy. Show this position is like an option; show debt holders have options on company; how can manager increase value of position?

The manager's ownership stake in the company is a call option with strike equal to the debt value. The debt owners have the short side. The manager can increase the value of the option by increasing the variability of its business.

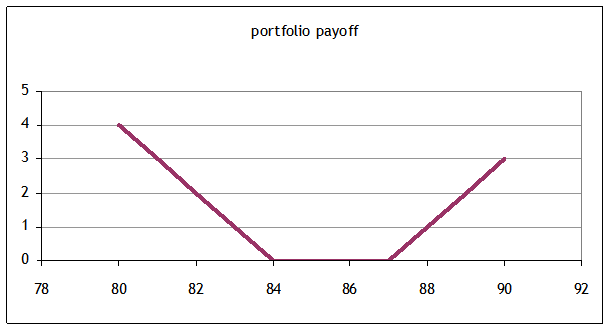

- A portfolio consists of two options on the same underlying stock, with the same expiration date in three months. The stock currently trades at $85. One option is a call with strike price of $87. The other option is a put with strike price of $84. Show the payoff graph for the portfolio.

The payoff graph is:

- An insurance company wants to hedge its position against hurricanes. The company believes that a Category-3 hurricane hitting a large city will cost it $500,000,000. It can buy "catastrophe bonds" that each pay out $2,500,000 in the event of a Cat-3 hurricane hitting the city. Each bond costs $10,000. The company would like to hedge at least 50% of its exposure. Should it buy or sell the catastrophe bonds? How many? What is the total cost? Or, the company could hedge using the city's municipal bonds, which would decrease in price if a hurricane struck. Explain the advantages and disadvantages to this alternate hedging strategy.

To hedge half of its exposure, or 250,000,000, would need to purchase 100 of these cat bonds, at a cost of 1,000,000. Hedging with munis would give less direct hedging since those could move downward for other reasons (the city's fiscal position).

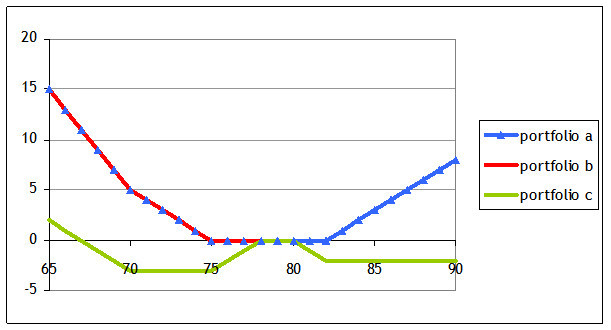

- A riskless bond pays 4% per year (compounded continuously). A stock has 25% volatility over a year. The stock's current price is 80. Your portfolio is long with 2 puts with strike prices of 75 and 70 and long one call with a strike price of 82. All these options have three months to expiry.

- Draw a payoff graph for the portfolio.

- Next a short call position, with an at-the-money strike, is added to the portfolio (same expiry). Draw the new payoff graph for the portfolio.

- Then a short put position is added, with a strike of 78 and 3 months to expiry. Draw the new payoff graph.

See Excel sheet.

- A bank has written 1000 calls on stock ABCD. These calls expire in 6 months and have a strike price of 15. ABCD's stock currently trades at 16. The portfolio of calls is currently worth 1956.88. The bank believes that the stock will be less volatile in the future: five percentage points less volatile than current option prices imply. What strategy of long/short positions in options, riskless bonds, or stock would allow the bank to profit from this knowledge? Explain how risky each strategy is.

If the stock becomes less volatile then the option price will decline; the bank can profit by shorting calls.