|

Homework 5 Possible Solutions

K Foster, Options & Futures, Eco 275, CCNY, Spring 2010 |

|

|

- Please complete Assignment

Question 10.19 in

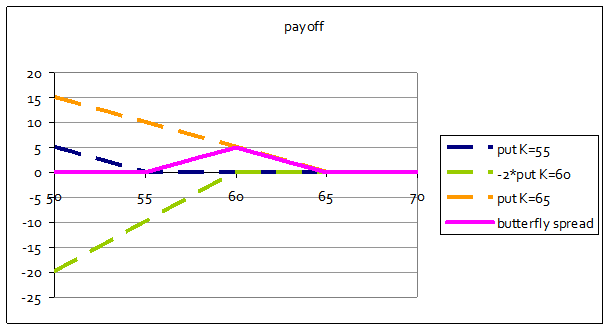

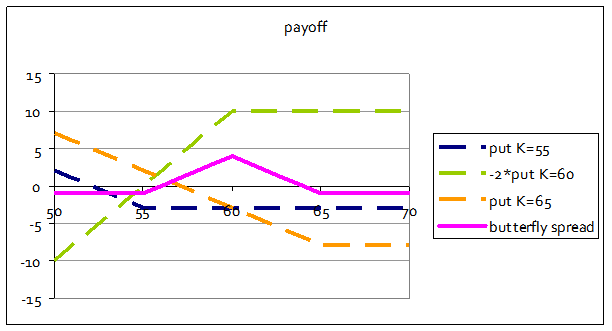

Three puts with K=55, 60, 65 have prices 3, 5, 8. Show profit to butterfly spread.

The Excel sheet has the table. This is the graph of the payoffs (not net profit)

The net profit is

- Please complete Assignment

Question 10.21 in

- one share plus ATM short call

- two share plus ATM short call

- one share plus ATM 2 short calls

- one share plus ATM 4 short calls

- Please complete Assignment

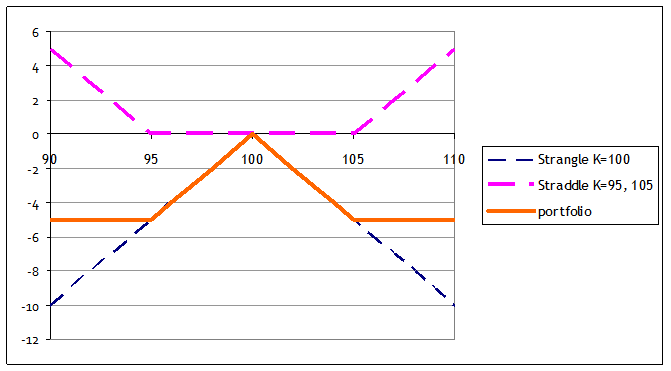

Question 10.23 in

Payoff to a long strangle and short straddle (both have same maturity).

And the profit would simply shift the net line upward.

- I am considering an investment in the country of Cunystan, which uses currency called the "zing". Since my home country offers interest rates of just 1.5%, I am looking to get higher returns. You are my portfolio manager, whose expertise I depend upon. The currency markets allow investors to buy and sell zing at a spot rate of $1 to 70 zing, and buy and sell forward (in one year) at a rate of $1 to 75 zing. Cunystan government bonds pay a riskless interest rate of 4% in one year (the zero rate, assuming discrete semiannual compounding). What investment strategy would you recommend, in this situation?

If

I invest $100 at home I get = 101.51.

If instead I invest in zing, I buy 7000 z today, invest it to get

= 7282.80, then convert back to dollars to get

$97.10

not a good investment! The higher interest rate is balanced by the

currency depreciation (hopefully you remember this from your baby econ classes!).

- A stock can

be modeled with a one-step discrete-time tree so that after one month the

stock, currently trading at $70 per share, will be worth either $75 or $60

(note that this is asymmetric).

Assume that the riskfree interest rate is 3%.

- Find the value of an at-the-money call.

- Find the value of an at-the-money put.

- Verify that put-call parity holds.

- Find the risk-neutral probabilities of up and down movements.

- What value

of (shares of the stock) make a riskless portfolio when combined with one short call? With one short put?

- Why are

these values of different?

Find

the risk-neutral probabilities by setting so

. So use these risk-neutral probabilities of p=68%

and (1

p) = 32% to value the ATM call & put. The call pays out 5 in "up" and

zero if the stock goes down so its PDV is

= 3.390.

The put pays out zero in "up" and 10 in "down" so

its PDV is 3.191. Put-call parity is c +

Ke-rT = p + S0, so verify that 3.390 + 69.796 = 70 +

3.191. If we use the Δ method instead,

then we find that a portfolio with Δ shares and one short call would have

payoff of 75Δ

5 in up and 60Δ in down. Set these equal so 75Δ

5 = 60Δ and Δ = 1/3. With the put instead, the payoffs would be

75Δ = 60Δ

10; so for a put Δ=-2/3. These values are different because the

payoffs of the put and call are opposite, so a hedge needs opposite holdings of

stock.

Note: you could use

discrete instead of continuous time discounting but that would mean, assuming

semiannual rates, using .

- Consider a one-step tree model, where each step is one month. Consider a stock currently trading at 1.25 but which has highly asymmetric possible returns: if the stock goes up it will quadruple in price to 5; if it goes down it will drop by one-quarter to 0.3125. A put option has a strike price of 2. Assume the risk-free interest rate is 2%.

- What does the model imply is the value of this put option?

- If the put option is actually priced at 1.25 (an odd coincidence that the stock value and option value are the same!), what values of "up" and "down" would produce this price?

Find

the risk-neutral probabilities by setting so

= .246 so (1

p) = 75.4 %.

A put option pays 1.6875 if the stock goes down, so the risk-neutral

valuation implies that it is worth

= 0.483.

If the put option were priced at 1.25, this would imply, if we decide

that "down" can never be negative, an "up" value of just 2.