|

Lecture Notes 5, Option Values (Ch 9) & Trading Strategies (Ch 10) K Foster, CCNY, Spring 2010 |

|

|

Learning Outcomes (from CFA exam)

Students will be able to:

§ determine the minimum and maximum values of European options and American options;

§ calculate and interpret the lowest prices of European and American calls and puts based on the rules for minimum values and lower bounds;

§ explain how option prices are affected by the exercise price and the time to expiration;

§

explain putcall

parity for European options, and relate put

call

parity to arbitrage and the construction of synthetic options;

§ contrast American options with European options in terms of the lower bounds on option prices and the possibility of early exercise;

§

explain how cash flows on the underlying

asset affect putcall

parity and the lower bounds of option prices;

§ indicate the directional effect of an interest rate change or volatility change on an option’s price.

From

Notation:

C value of American call option (sometimes distinguish between C0 and CT, the value now and value at maturity)

P value of American put option

c value of European call option

p value of European put option

Six important factors affecting option prices:

- Current stock price, S0

- Strike, K

- Time to expiration/maturity, T

- Volatility, σ

- risk-free interest rate, r

- dividends of stock over T

Look at each:

First, the value of an

option depends on the spread between

S and K a call is worth max(ST

K,0) while a put is worth max(K

ST,0). So if the stock price, S0, rises

while K is constant, then this increases the value of a call but reduces the

value of a put; if the stock price falls while K is constant then the call

price falls while the put price rises.

It works vice versa for K.

Generally higher stock prices result in higher call prices but lower put

prices.

Time to expiration is generally a positive factor, certainly for stocks without

dividends. (If substantial dividends are

paid, which reduce the value of a stock on the day after, then the dividend

schedule can affect the option value.)

American options, which can be exercised anytime, are certainly always

worth more when there is a longer time to expiration more choice can never be bad!

Volatility (or uncertainty) is a positive factor. This might seem odd unless you remember that options are basically providing insurance, and it certainly seems sensible that more uncertainty raises the value of insurance.

The risk-free interest rate affects the present value of the payoffs to options (since the payoff will be received in the future, a higher rate means a lower present value). However since the expected future price is influenced by the risk-free rate, a call would be worth more while a put would be worth less.

Since dividends reduce the value of a stock on the day after, higher dividends raise the value of a put and lower the value of a call.

Upper Bounds for Option Prices

A call gives the right to buy the stock so it can never be worth more than the stock price; c ≤ S0 and C ≤ S0

A put gives the right to sell at K so it can never be worth more than K, p ≤ K and P ≤ K; in fact p ≤ Ke-rT.

Lower Bounds for Option Prices

These are trickier. For a call, consider 2 portfolios: portfolio A buys a call, c, and invests an amount of cash Ke-rT. Portfolio B just buys a share at S0. The value of portfolio A will be, at date T,

max(ST

K,0) + Kerte-rT = max(ST

K,0) + K = either ST or K,

whichever is bigger, so = max(ST,K).

Portfolio B will evidently be worth ST at the end of the period so portfolio A will always be worth more than portfolio B (or equal in value to it), or

c + Ke-rT ≥ S0

so c ≥ S0 Ke-rT

For a put, on the other hand, consider 2 more portfolios: portfolio C buys a put and the stock, so p + S0, while portfolio D invests the cash Ke-rT. The value of portfolio C will be, at date T,

max(K ST,0) + ST = either K or

ST, whichever is bigger, so = max(ST,K).

Portfolio D will be worth K at the end of the period, so again portfolio C is always worth more than D (or is worth the same amount), so

p + S0 ≥ Ke-rT thus p ≥ Ke-rT - S0

Put-Call Parity

We can also note that portfolios A and C have the exact same value, max(ST,K). So their values must be equal, so

c + Ke-rT = p + S0

or

c p = S0

Ke-rT.

This connects the values of

the call and put options a connection that seems reasonable since both

depend on the properties of the very same underlying stock. The excess of the value of a call over a put

depends on the excess of what we can interpret as the expected present value of

the "intrinsic" value, S

K.

We can get some idea of the

rationale behind this by thinking of the value of a call and put, just moments

before the exercise date. A call is

worth the excess of the stock price over the strike while a put is worth the

excess of the strike over the stock price.

So just a moment before exercise, c = max(ST K,0) and p = max(K

ST,0), or to write in greater

detail,

and

so that c p = ST

K in either case. Put-call parity is just the present value of

that relationship.

For American options, a similar result (for non-dividend stocks) can be derived:

S0 K ≤ C

P ≤ S0

Ke-rT.

Early Exercise of American Options

For non-dividend stocks, an American call is never optimally exercised before the expiration date. There are two reasons for this: that the insurance value should be kept for the duration of the period (you would never want to pay for a year of insurance but then cancel after 6 months!) and the fact that the strike price must be paid, so the time value of money indicates that we want to defer that payment.

However for non-dividend stocks, an American put might be optimally exercised early, because there is a maximum of the put value: if the stock price goes to zero then the put is worth K.

Dividends make the arguments above a bit more Byzantine but don't change the basic intuition.

|

Trading Strategies |

|

|

From

Combining a stock position

with an option allows investor to put a cap or floor on payoff. But this has a more subtle implication it can allow us to take another view of

put-call parity.

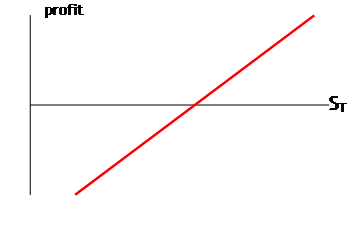

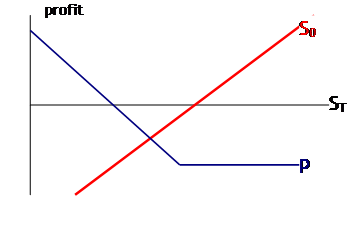

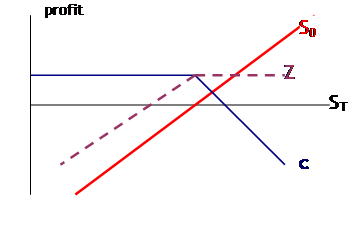

Consider the profit to buying a stock and buying a put with strike K. The profit function of the stock, S0, is

and the profit function for the put, p, purchased at some cost (so that the investor loses some money if the stock price rises and the put is not exercised) is

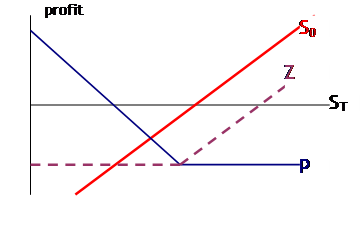

so the profit to the combined function is the purple line:

.

.

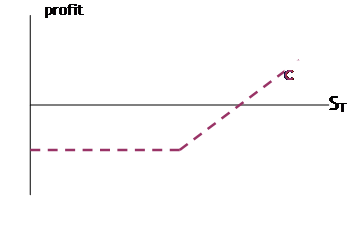

The profit to this combination, which I've labeled "Z", looks remarkably like the profit to buying a call, c, at some cost:

.

.

What could cost be? Recall our formula for put-call parity, that for a stock that does not pay dividends, p + S0 = c + Ke-rT. What is the payoff to a portfolio with one put and one share of stock? That's the " p + S0" part. What is it equal to? A call, "c", plus some amount of cash, " Ke-rT ". So we could also derive our formula on put-call parity from the equivalence of the payoff functions.

This is a taste of a more

general result: if two portfolios give the same payoff functions, then if they

do not have the same current market value then there are arbitrage

opportunities (which, in a perfectly functioning market, would be absent). Put another way, if markets are efficient

then two portfolios that give the same payoffs should have the same value. We'll do some work to show that any payoff

pattern can be replicated with combinations of puts and calls in order to show

that, once we've gotten valuations for puts and calls, we've done all the work

that's necessary any other portfolio can be valued!

We can go through to

re-order the put-call parity equation and figure other payoffs. Rearrange so that S0 c = Ke-rT

p and this says that a short put ("-p")

with some amount of cash has the same value as a long stock ("S0")

and short call ("-c") position.

This diagram is:

where now "Z" looks like the payoff function to a short put. We can keep on rearranging to show that the long put and short call can also be replicated.

Market participants have named a variety of different combinations of options. Among them are:

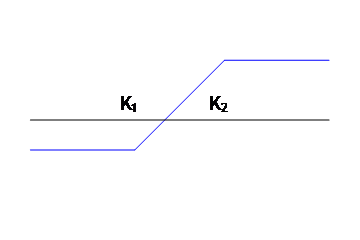

- Bull

Spread: buy a call at K1

and sell a call at K2 (

- Money-ness determines the cost

- if both K1 and

- if K1 is initially in the money

but

- if both are in-the-money

- Can also be replicated with puts: buy a put at

K1 and sell at

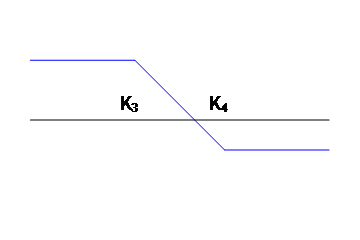

- Bear Spread: buy a put at K4 and sell a put at K3 (K3 < K4)

- Can be replicated with calls as well

- Box Spread

- combines bull spread and bear spread, but K1=K3

and K2=K4 so the payoff is always (K1).

- if cost is different from (present value of) payoff then arbitrage

- Butterfly Spread

- options with strike prices K5, K6, K7 (K5 < K6 < K7)

- buy call at K5

- sell two calls at K6

- buy call at K7

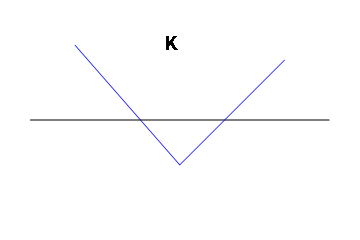

- Straddle

- Buy a call and buy a put, both at K

- Profit if large moves in either direction

- straddle write or top straddle has opposite

payoffs profit if stock price moves little but loss if stock goes up or down

- Strip buys one call and two puts; strap buys two calls and one put (all with same strike) will skew the payoffs

- Strangle buys a put with strike K8 and a call with strike K9 (K8 < K9)

- All of these were assumed to use options with same expiration date but "calendar spreads" use different expirations to further complicate the position payoffs

If options are available at any given strike price, then we can replicate ANY payoff function using calls and puts.