|

Midterm

Exam K

Foster, Options & Futures, Eco 275, CCNY, Spring 2010 |

|

|

- (10 points) You're going to buy

corn futures; each full-sized contract is 5000 bushels, while

mini-contracts are 1000 bushels (delivered to a few locations in Illinois). Currently the contract for July 2010

delivery (on the 14th of that month) trades at 375 (cents per

bushel).

- How much does a single

full-sized contract cost? A

mini-contract?

- Given interest rates of 2.5%,

what range of prices would not present arbitrage opportunities?

- Initial margin is $1350 so

assume you buy one contract with only that margin amount. The maintenance margin is $1000. How large of a price decline would

trigger a margin call?

- (20 points) You have a portfolio

with calls and puts on oil contracts; all of these options are

European. The current oil price is

$80.68/barrel. You are long 10

calls with strike of 82 and short 8 calls with strike of 84. (Contract size is 1000 barrels in each;

each option brings the right but not the obligation to buy 1000

barrels.) You own 5 puts with

strike price of 81 and 5 puts with strike price of 80. You are short 7 puts with strike prices

of 83.

- Draw the payoff graph for your

portfolio.

- If you bought 10,000 barrels

(or 10 contracts) at a price of 80.50/barrel, how would the payoff graph

change?

- (25 points) You are considering

whether to buy an at-the-money European put, expiring in a month, on a

stock that is currently worth 50.

After one month assume the stock will be worth 55 or 45. The risk-free rate is 2%.

- What are the risk-neutral

probabilities of the stock rising or falling?

- What is the delta for the put?

- What is the fair value of the put?

- (20 points) The Greek government has seen

prices of its bonds fall dramatically.

Consider two (fictitious) bonds; both pay 100 semi-annually. One is an on-the-run 5 year bond with

just 1.5 years remaining (3 remaining payments); the other matures in 3

years and also pays 100 semi-annually.

- As of September 2009, the first

bond traded at a price of 292.65.

The second bond traded at a price of 662.61. Assuming discrete semi-annual

compounding, what was the implied zero rate for 1.5 years?

- What was the forward rate from

1.5 to 3 years?

- By March 2010 (6 months late),

- What is the forward rate from 1

to 2.5 years?

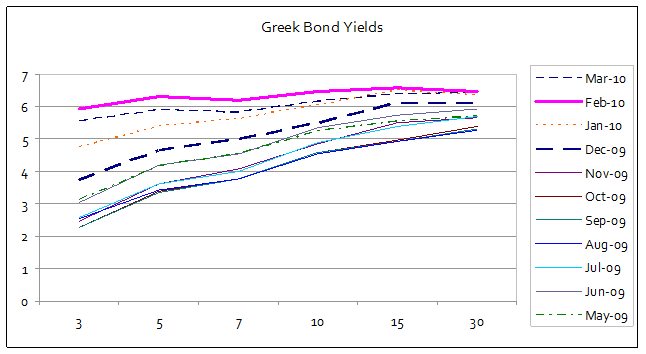

- Actual Greek bonds saw the

yield curve compact, as short rates rose substantially while longer

yields rose by less; the graph below (data from Greek Central Bank) shows

yields on 3 – 30 year bonds.

Explain why this might be so.

- How has the duration of these

bonds changed?